Where Brands Grow

For years, the ecommerce story focused on two aisles. The steady reach of retail and the excitement of DTC. But as shoppers change how they buy, marketplaces have grown into the third aisle that few brands can afford to overlook.

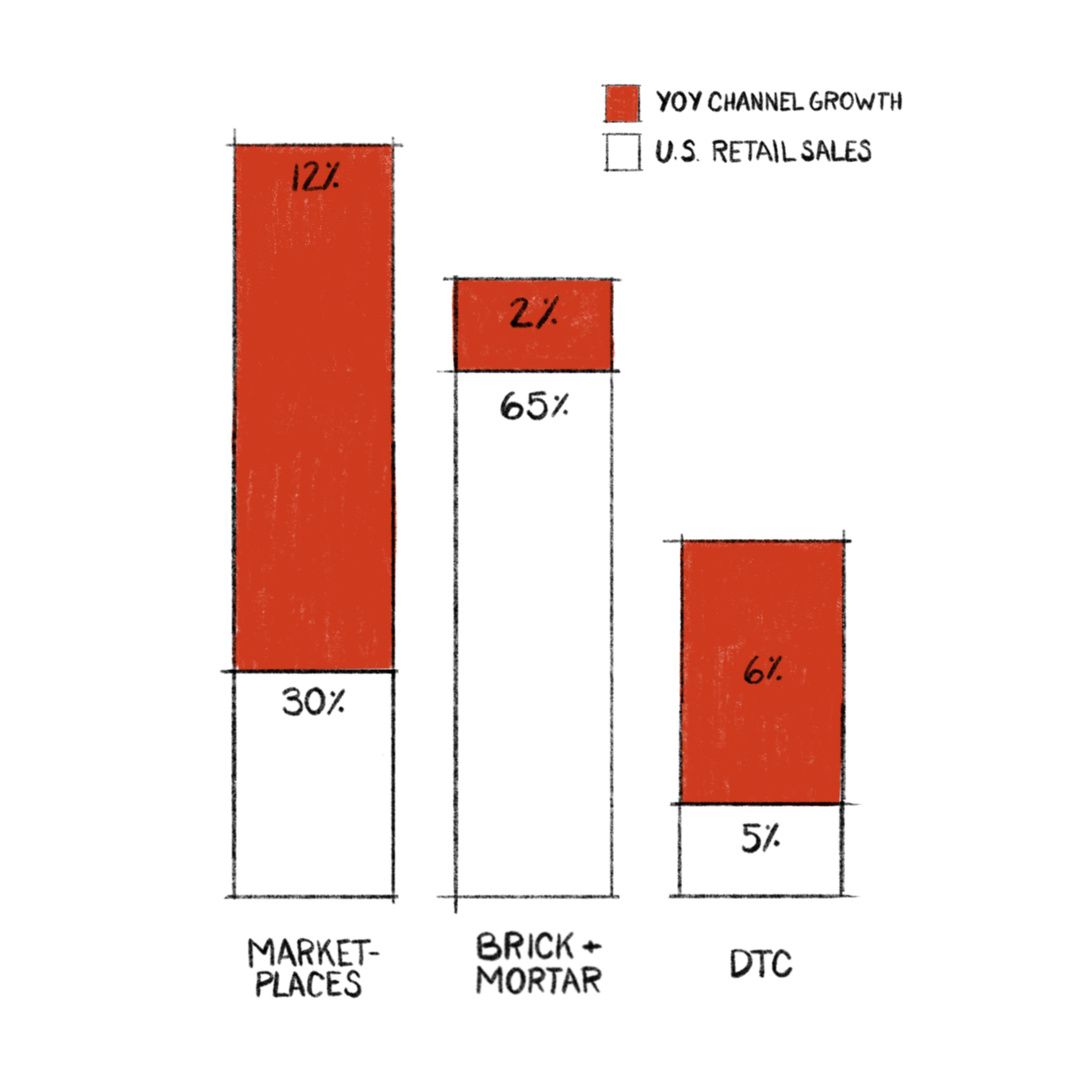

When you remove grocery and fuel from the picture, the pattern becomes clearer. Roughly two-thirds of discretionary spending still happens in stores, and that part of the market grows only a point or two each year. About one-third now flows through marketplaces like Amazon, Walmart, and Target, which continue to expand at a pace near 12% annually. The smallest slice runs through brand-owned DTC sites, which are still growing, but more slowly, closer to 5-7% gains each year.

Those numbers line up with government data and industry reports. They show what most founders already feel. Marketplaces are no longer a side channel. They are where real growth and buying intent live.

Yet most marketing plans are still built for aisles one and two. Budgets favor awareness and acquisition, not intent and conversion. The outcome: dollars chase impressions while marketplaces quietly drive the revenue curves.

The Budget Gap

When you compare how brands spend with where shoppers buy, the gap shows up fast.

Half or more of most budgets go toward trade spend, shelf space, and co-op programs that support the slowest-growing channel. Another third goes toward social and search campaigns that push shoppers to DTC sites, where conversion rates often sit at two or three percent.

The smallest slice of most marketing plans covers marketplaces, even though conversion rates often hit 10% or higher. The channels that deliver the highest return usually get the least investment.

Why The Third Aisle Matters

Marketplaces do more than drive sales. They create signal. Every click and purchase helps a brand see what people actually buy, which listings convert, and what words pull the most traffic. Those signals shape packaging, pricing, and inventory decisions that improve performance everywhere else.

Each aisle still plays a role. Retail builds reach and familiarity. DTC builds loyalty and tests new ideas. Marketplaces turn all of that interest into action. They are where people compare, review, and decide.

A Better Balance

The goal is not to pick one aisle over another. It is to weigh them based on how shoppers actually buy. For most brands, that means shifting a modest share of budget (around 5-10%) toward marketplace readiness. Even small adjustments can deliver outsized returns.

Investing here improves the parts of the business that move fastest: retail media coverage, product page quality, and visibility where shoppers already start their search. These are the moments that convert interest into action.

Growth on marketplaces rarely comes from hacks or viral moments. It comes from execution. Clear images. Accurate titles. Reliable stock. Ads that show up where intent is highest. Brands that get these fundamentals right perform better on marketplaces and they perform better in stores and on their own sites too.

More teams are beginning to rebalance. They are moving spend toward the aisle that actually holds the demand. When marketplaces perform, every other channel benefits. Social traffic can feed marketplace listings, and strong reviews there can nudge a shopper to buy direct next time. It all works together when the system is aligned.

The Third Aisle is not an add-on anymore. It is where intent meets execution and where steady, durable growth continues to build.